Market Data Bank

Click image to enlarge

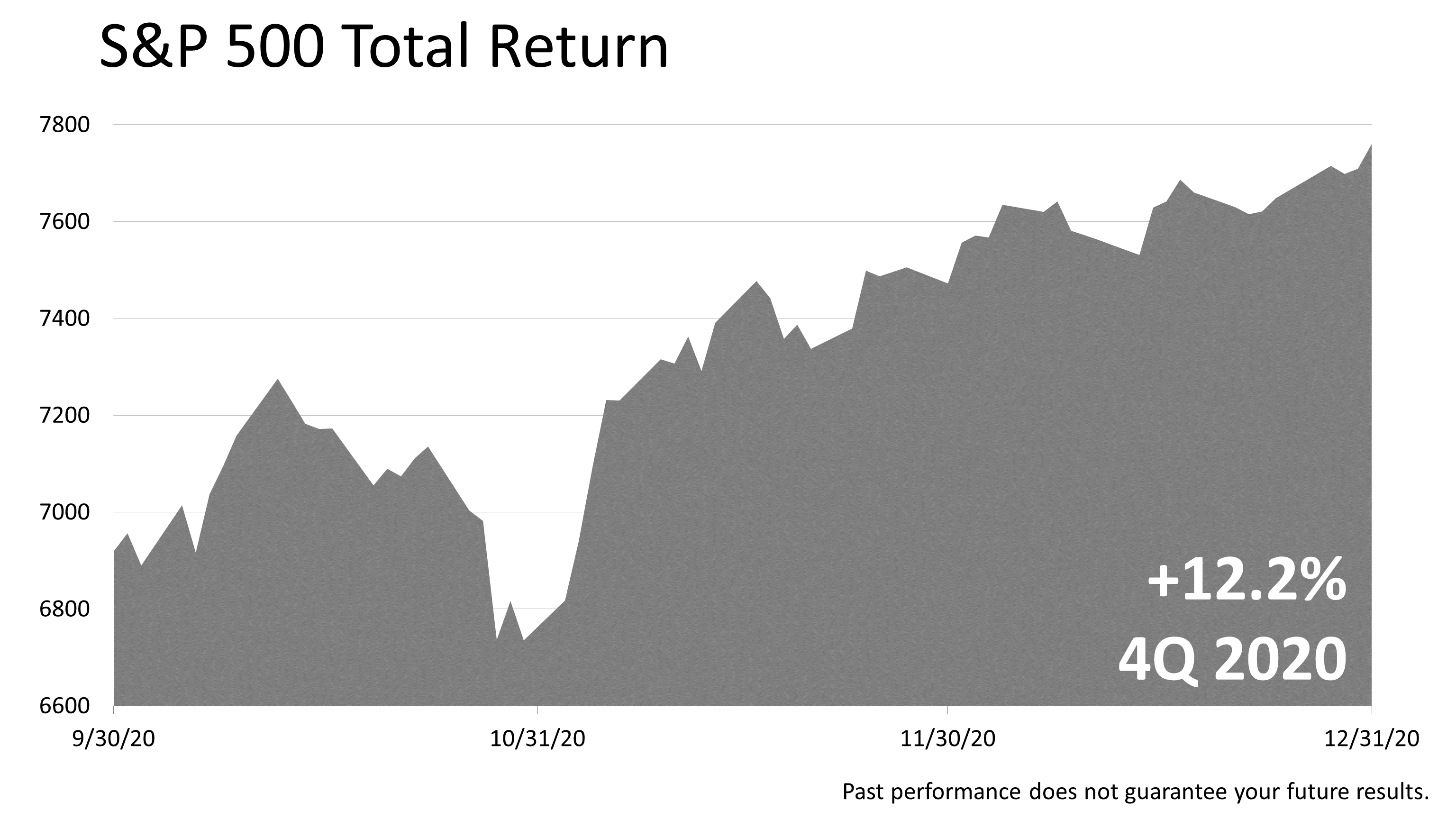

Stocks posted a +12.2% gain in the fourth quarter of 2020, following an +8.9% gain in the third quarter and a +20.5% gain in the second quarter of 2020, which followed the Covid bear market loss in the first quarter of 2020 of -19.6%.

Click image to enlarge

Let’s look at where we are today from an historical perspective.

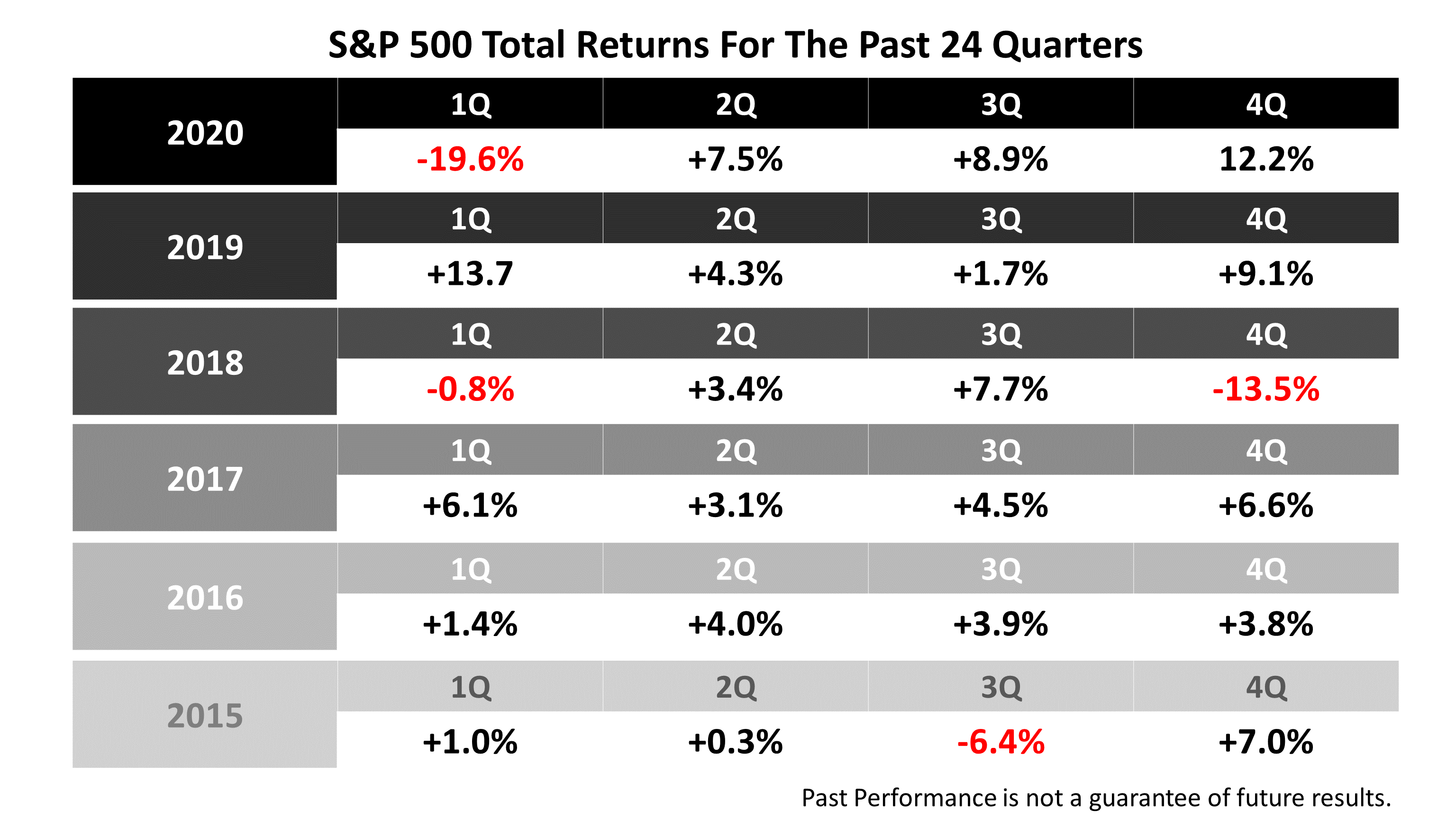

This table shows the last six years of quarterly results.

It was six years of a rising bull market. Actually, it was the second half of the last bull market, which was 128 months long.

It was the longest bull market in modern Wall Street history, which goes back close to a century.

Then, after that long expansion and bull market came the initial outbreak of Covid in the first quarter of 2020, which resulted in a loss of -19.6%.

The 10-year, eight-month expansion was the longest in post-War history, and it fueled the biggest bull market in post-War history.

Now, past performance is no guarantee of your future results; the future always is uncertain, and what happens is never expected.

But it is good to remember that the 10 year, eight-month expansion followed a global credit crisis in 2008 and what history now records as The Great Recession—the worst recession in modern history.

Point is, as you look at the current peril facing our society and the risk of the stock market currently, keep in mind that the foundation of every economic expansion and bull market for decades has been built on the shaky planks of an economic downturn or disaster.

Click image to enlarge

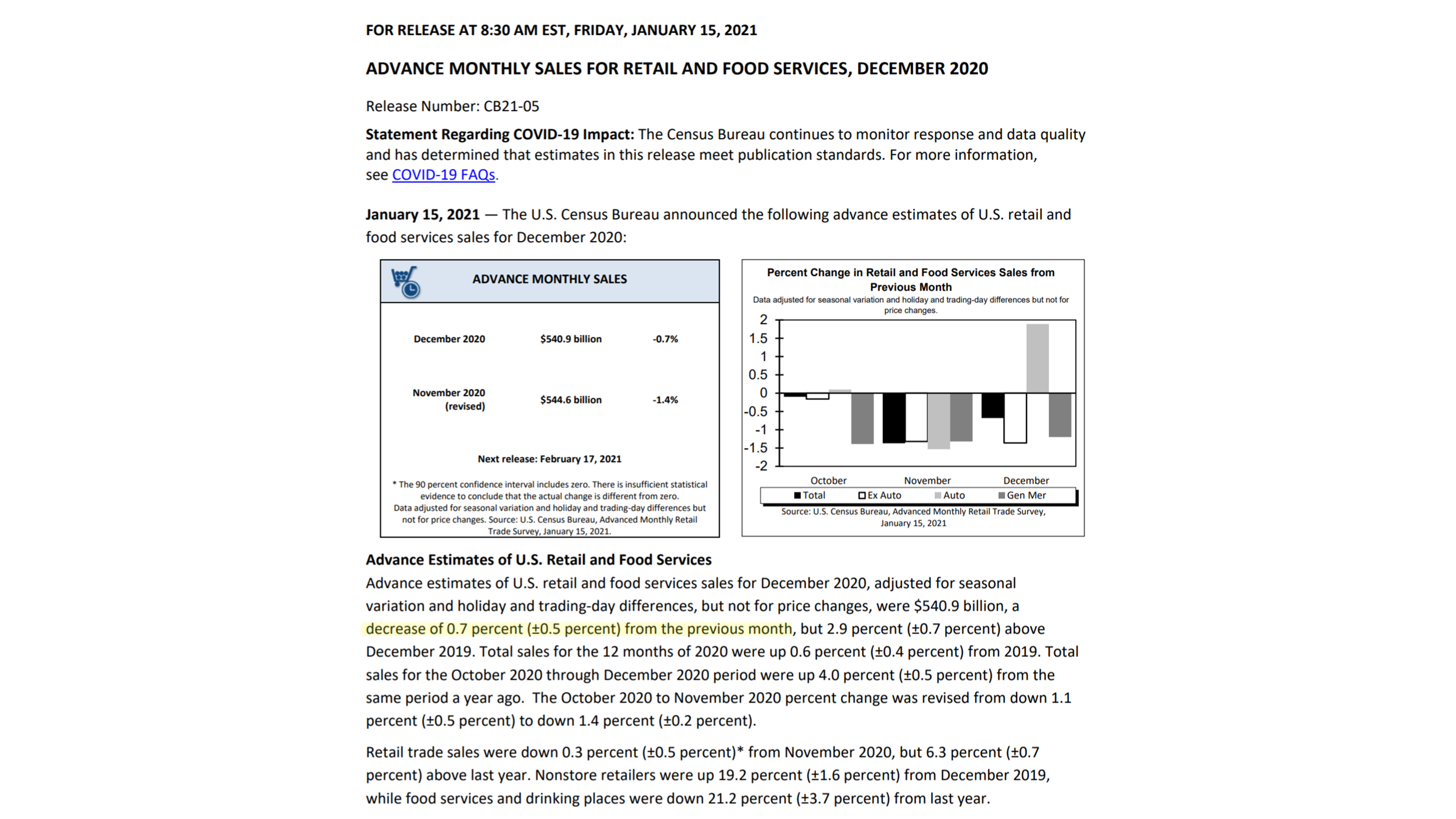

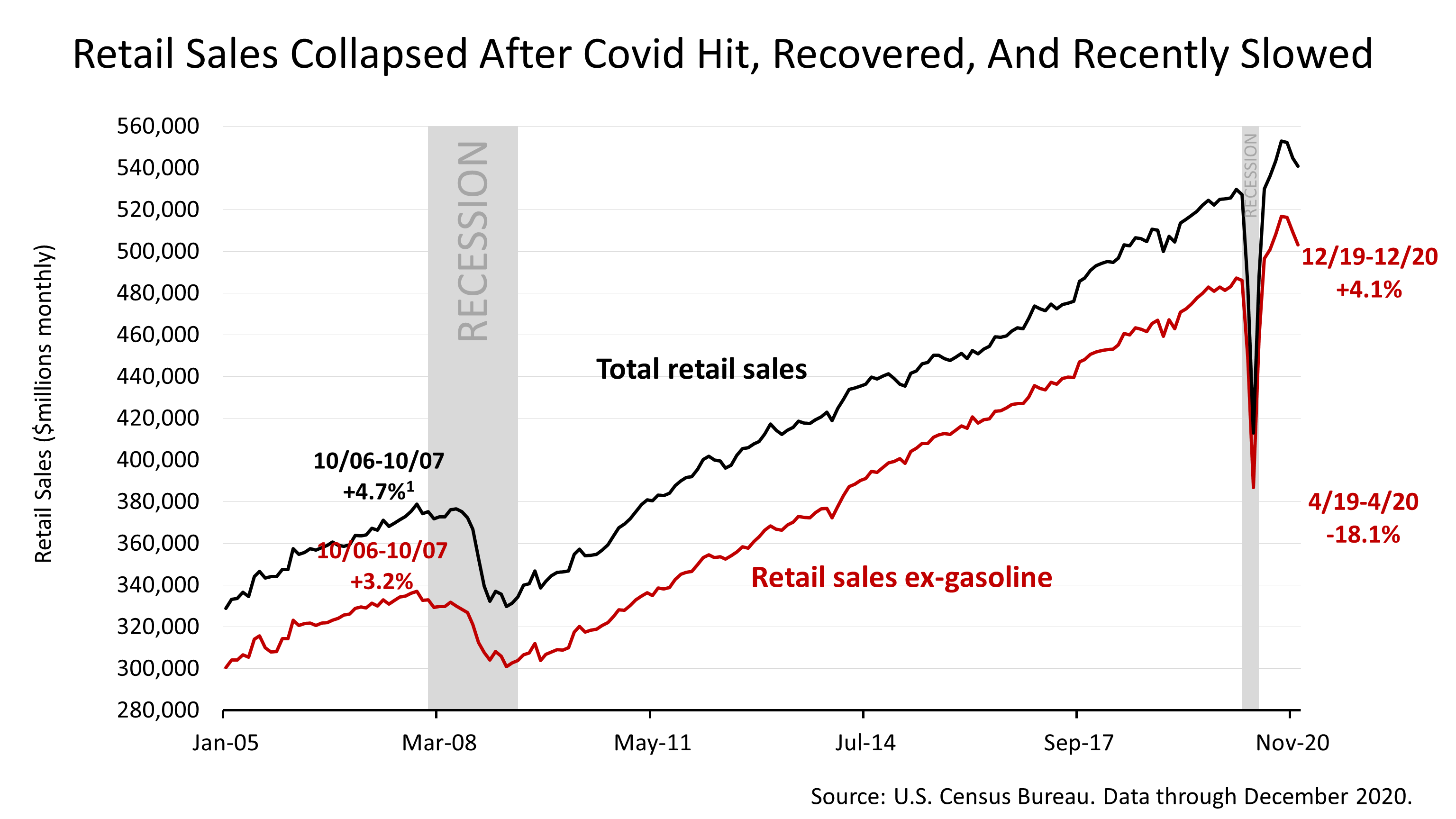

The latest economic data—like December’s retail sales—reflect the uncertainty that accompanies recoveries.

It’s worth looking at how applying a long-term historical lens to the data makes a big difference in examining financial and economic news.

Compared to November 2020, retail sales, which account for 30% of the total economy, declined by seven-tenths of 1% in December.

Click image to enlarge

The red line, which shows retail sales, excluding gasoline because its volatile price distorts retail sales trends, declined sharply in December, by seven-tenths of 1%.

Retail sales comprise 30% of the total economic output of the United States, which, you might remember from high-school, is gross domestic product.

The sharp dip in retail sales is evidence that the post-COVID recovery that began last April has lost strength.

Click image to enlarge

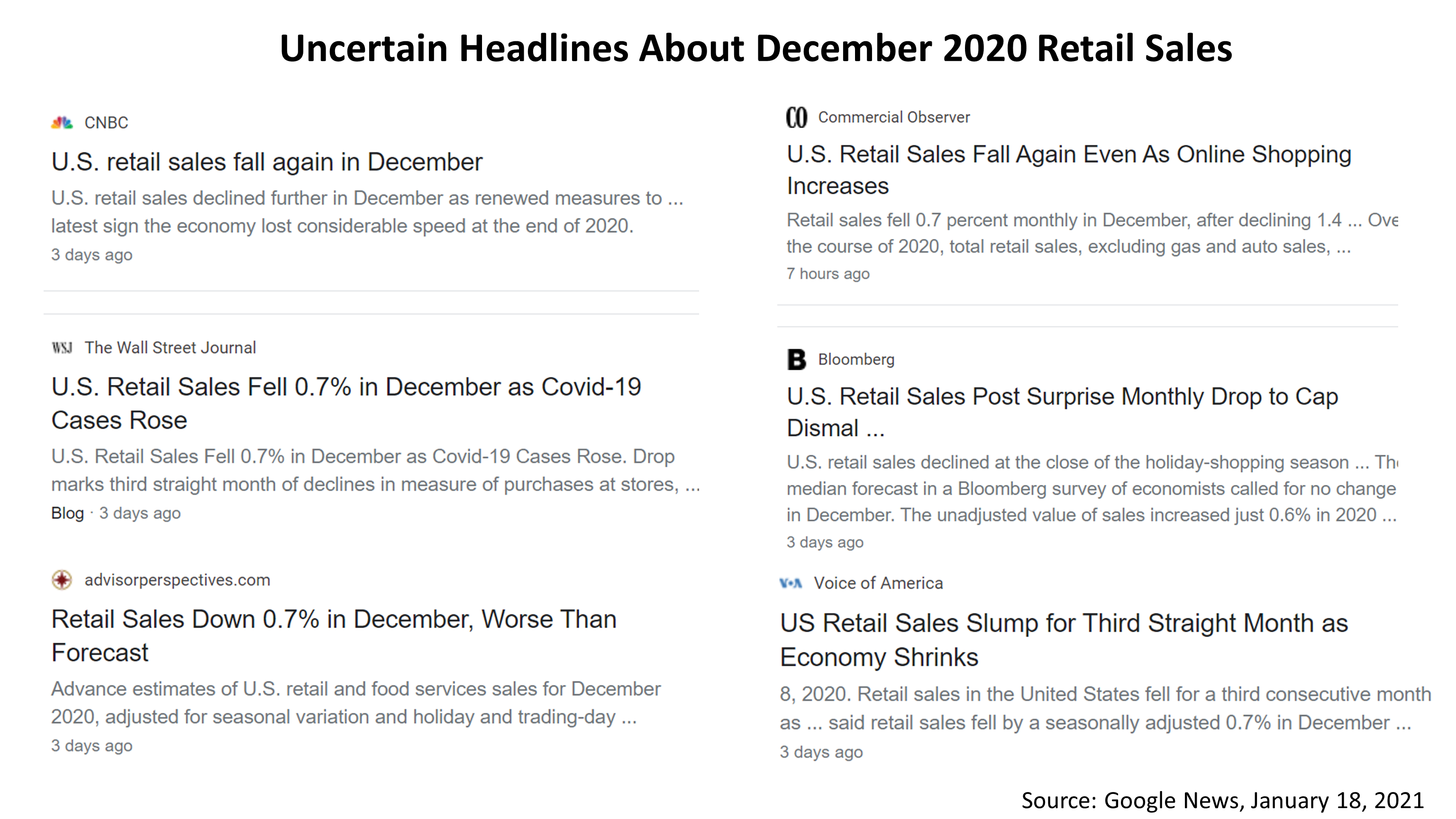

Now look at the headlines that followed the release of the retail sales numbers by the Census Bureau on Friday, January 15.

This is a search of Google for the term “U.S. retail sales December 2020.”

These were not cherry-picked but were the actual results of how the press covered the December retail sales.

Look at the negative impression of the economic news that it gives you.

This is actually a great example of the dilemma investors face in the internet age.

Investors will see fear-filled headlines like these and form opinions about the future of the economy and how to invest.

Click image to enlarge

Returning to this chart of retail sales for the past 16 years, compiled and illustrated by an independent economist for us, excluding gasoline in the 12-months that ended December 31st, 2020, retail sales gained +4.1%.

That compares to a +3.2% gain averaged during the previous economic boom leading up to the Great Recession.

To be clear, financial news reported by the media is typically not focused on the long-term trends that matter most to investors.

Because the financial media look at the economic news very differently from a professional investment advisor, presentations like this one are one way we can provide perspective on the financial and economic news.

Please subscribe to our news feed, which continually examines the latest economic and financial data through the prism of a long-term investor’s lens.

Click image to enlarge

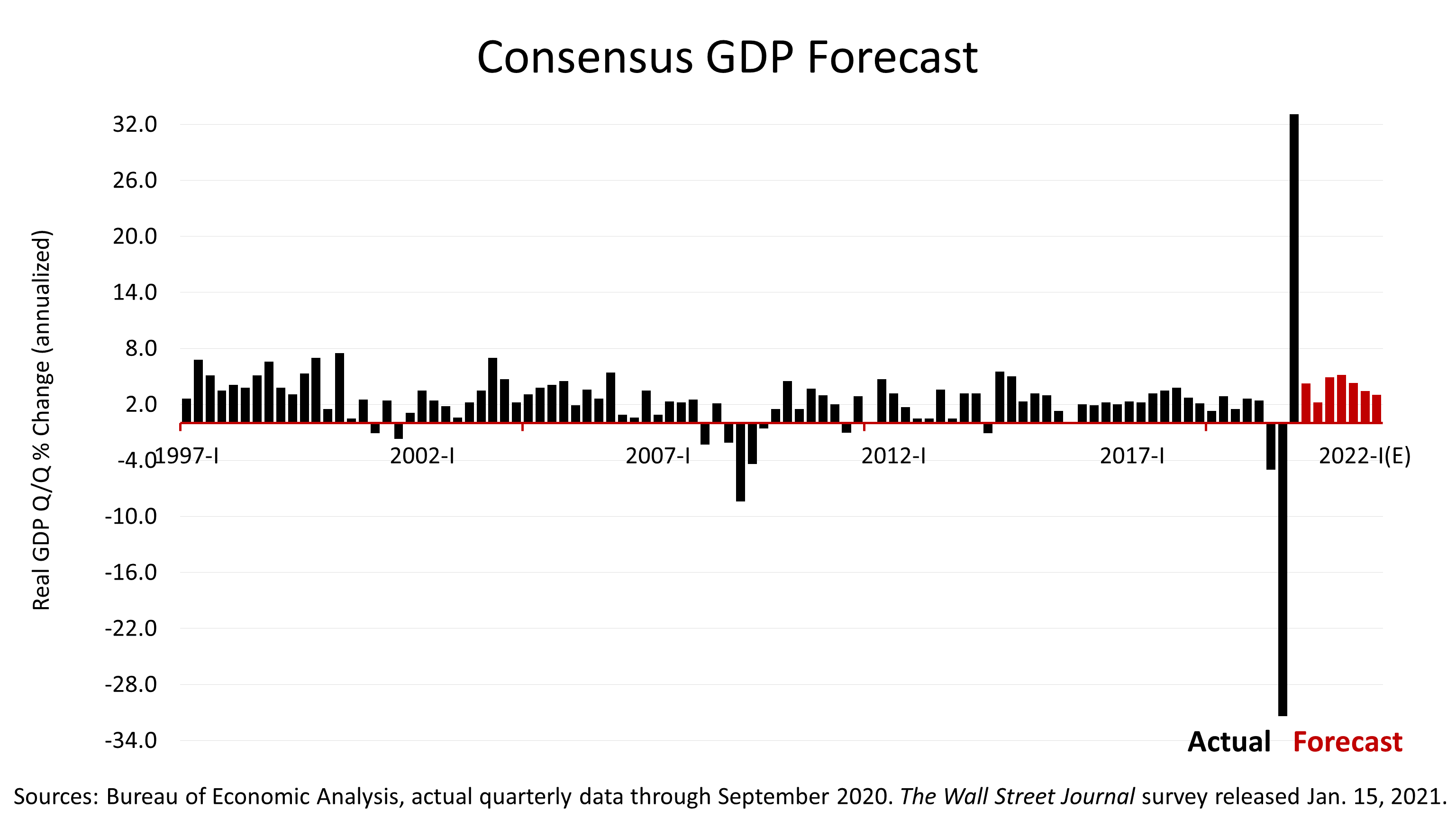

Despite the drop in retail sales in December, the consensus forecast of 60 leading economists surveyed monthly by The Wall Street Journal, released January 15, remained sanguine.

Economists expect that when the fourth quarter 2020 GDP figure is released in late January, the U.S. will grow by +4.3% in the quarter which ended December 31, 2020.

A +2.2% quarterly rate of growth is forecast for the first quarter of 2021, with significantly higher growth rates projected for the quarterly periods through the end of September 2022.

So, despite the bad news about December retail sales and other challenges to the economy, the U.S. is not expected to suffer a double-dip recession, according to the consensus forecast of the 60 leading economists surveyed by The Journal.

The point is that economic and financial data are easily misrepresented or presented without proper context.

As a professional financial advisory firm, we are committed to presenting you the full picture in presentations and communications like this.

Click image to enlarge

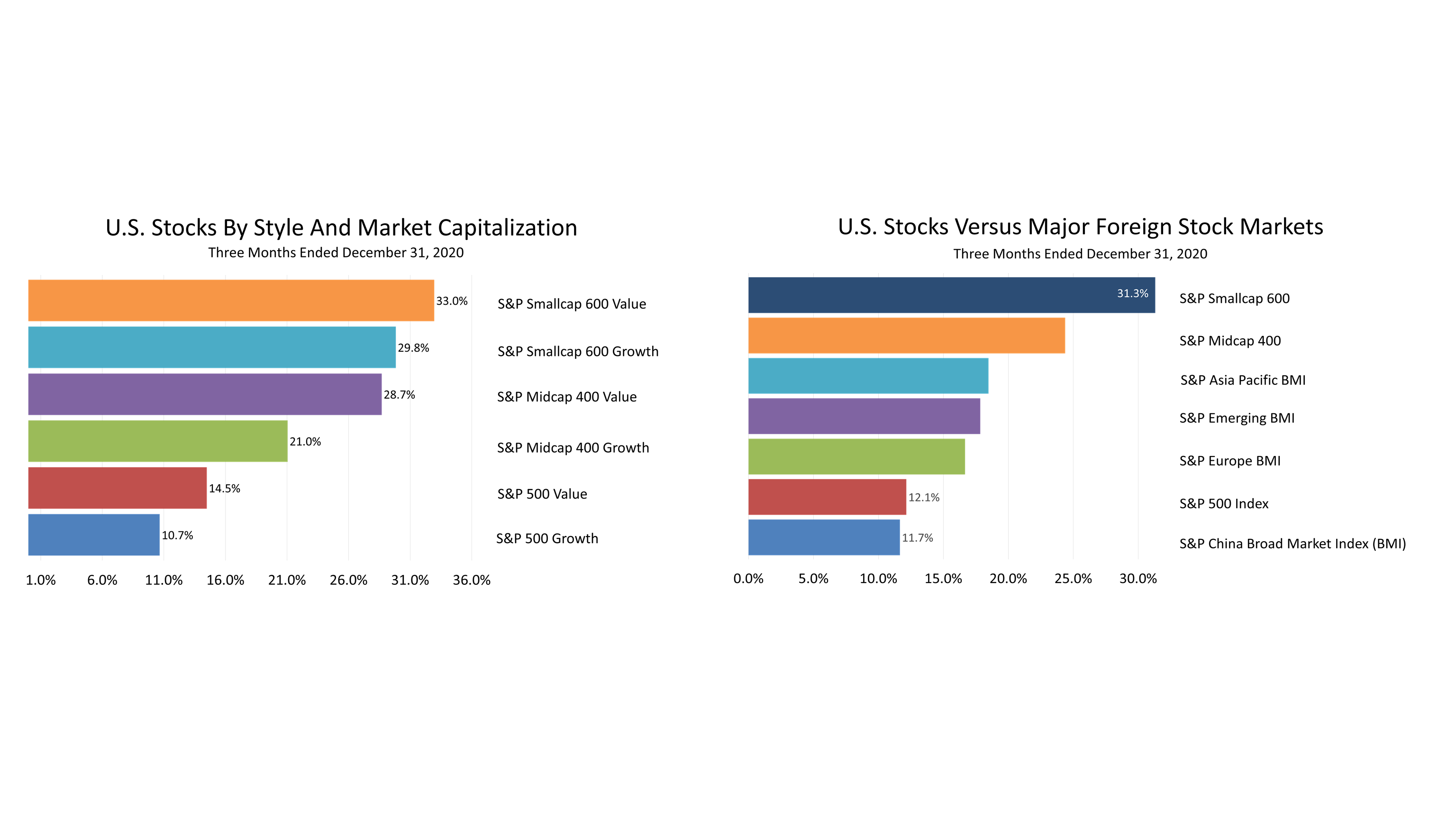

Can you spot the major shift in the market in these figures?

Normally, one quarter of data is not very helpful in understanding what’s happening in the investment markets, but this past quarter included a shift in leadership.

Click image to enlarge

The shift in the market is also seen in the result shown here. Can you see it?

Click image to enlarge

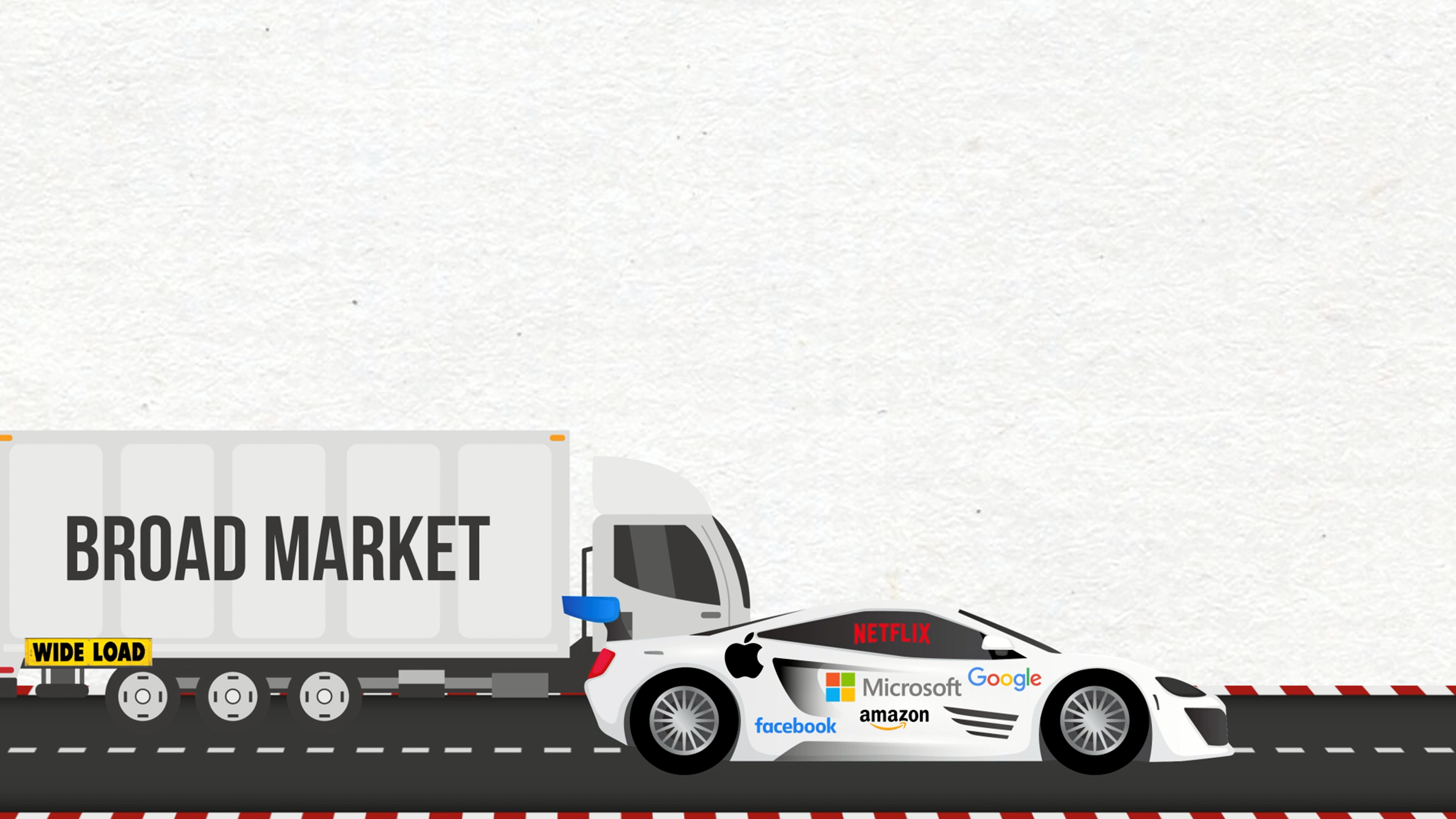

The stock market's performance was almost entirely determined by six companies in the S&P 500 in the first nine months of 2020: Facebook, Amazon, Apple, Netflix, Google, and Microsoft (FAANGM).

However, in the last three months of 2020, returns on the 494 other companies in the Standard & Poor's 500 index outside of the FAANGM outpaced the FAANGM.

Click image to enlarge

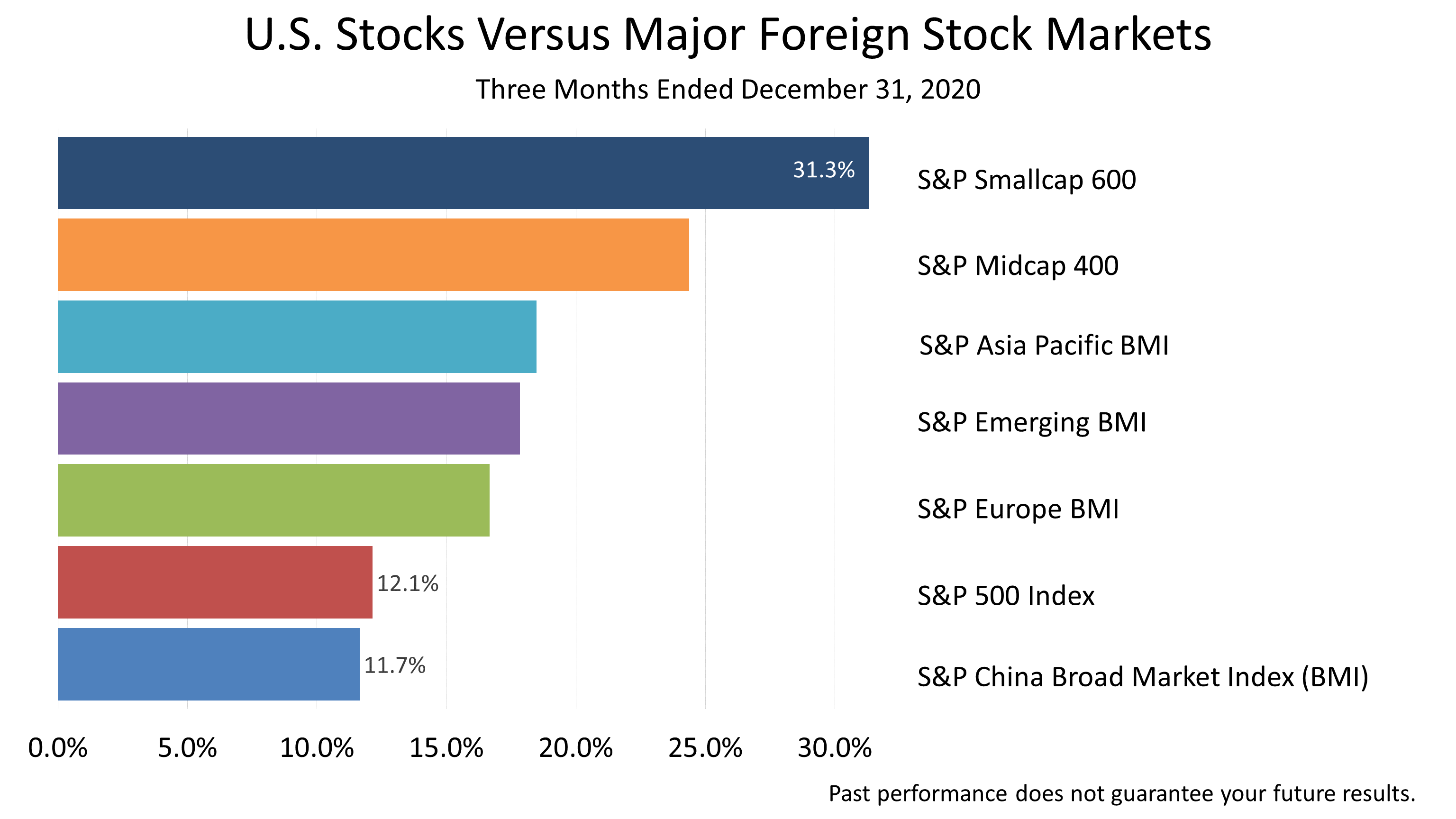

In the three months ended December 31, 2020, the S&P 500 index of large-cap stocks did not lead the U.S. market. Nor did it outperform foreign stock markets.

Instead of large-cap blue-chip companies showing the strongest returns, small-cap and value stocks were the outperformers.

That was contrary to what happened over the longer-term.

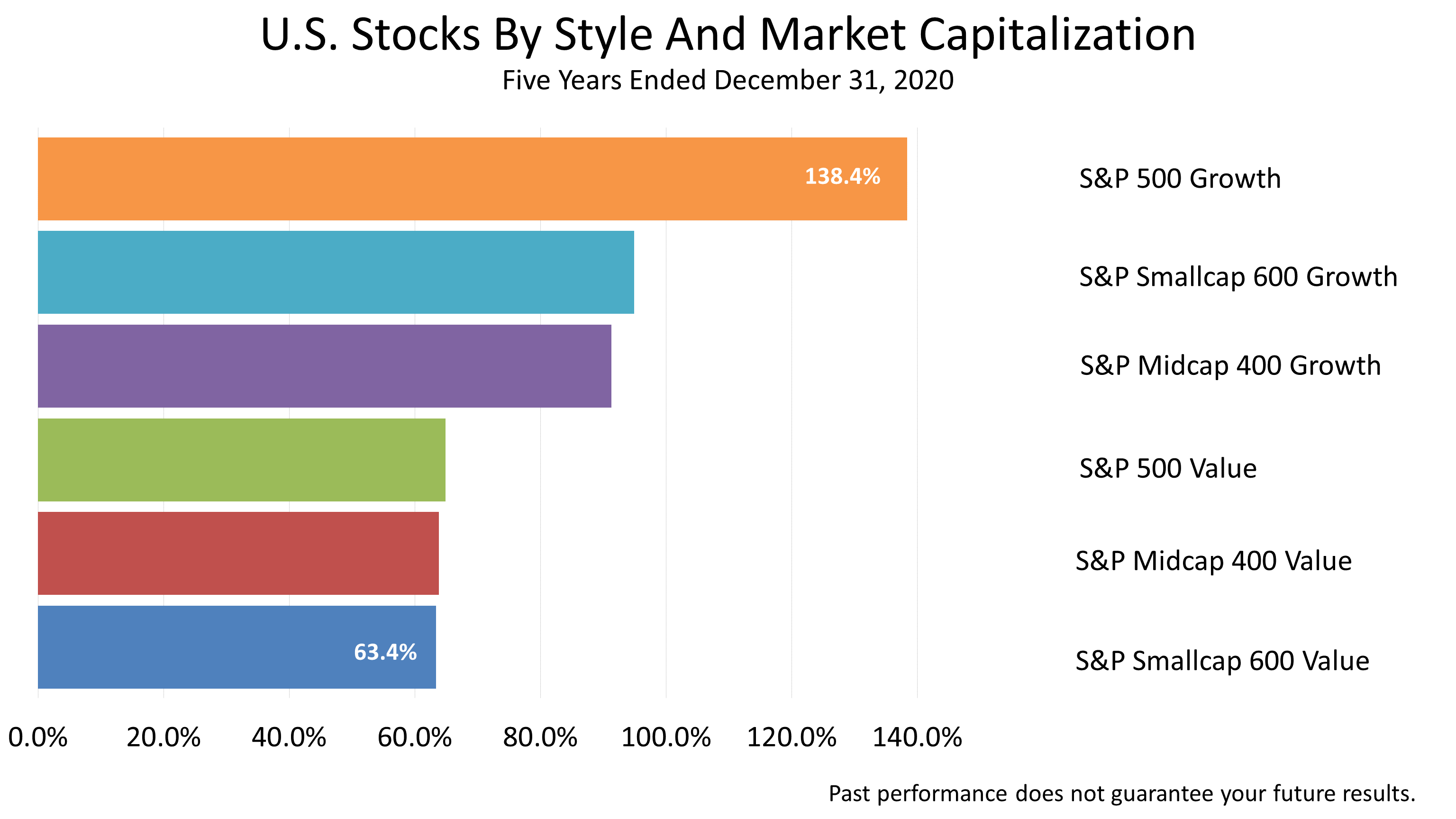

Click image to enlarge

Look at what happened over the past five years: the large growth companies returned +138%.

That’s more than twice as much as the gain on companies classified small, value-style investments.

The S&P 500 is a market-capitalization-weighted index, so the price of the widely watched benchmark of the financial strength of the United States is influenced more by the largest of the 500 companies in the index.

During the pandemic, Facebook, Amazon, Apple, Netflix, Google, and Microsoft—the FAANGM—grew more, and they became much more dominant in their influence as they drove the performance of the S&P 500.

While small businesses were crushed by the Covid epidemic and trailed the big six technology giants at the outset of the virus crisis, the other 494 companies in the S&P 500 index caught up in the final three months of 2020.

Click image to enlarge

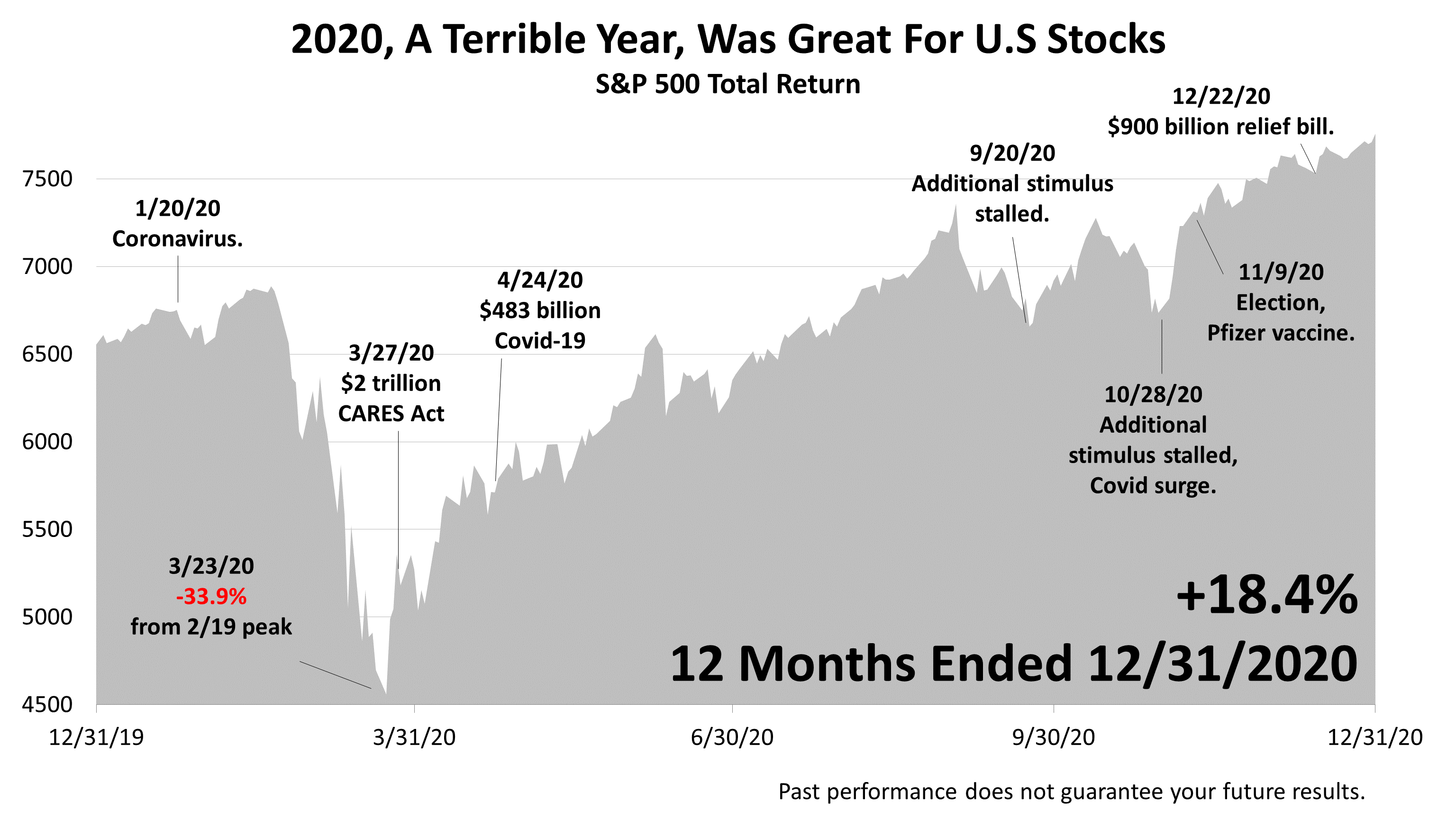

2020 was a terrible year, but stocks soared.

Actually, it was a great year for the S&P 500!

This 12-month period illustrates how investing is as unpredictable as the future.

It was a time when the advice of a professional could make all the difference in your portfolio.

At the outset of the Covid crisis, so many investors bailed out after stock prices began to drop.

Some investors dropped out after the S&P 500 dropped -10%, and some dropped when the price fell by -20% or -25%.

Ultimately, the bear market bottom of the Covid crisis came on March 23rd, 2020. The price of the S&P 500 bottomed after stocks lost -33.9% of their value.

At that moment in time, having a professional advisor to call—a coach for individuals who are ready to give up when things look bleak—proved to be extremely valuable.

Only by studying the history of economics and investments can you know enough to feel confident to advise a client what to do in uncertain times.

Living through financial crises also adds important perspective, as does professional training and continuing education.

Sometimes, being an advisor is not about telling people what to do, but helping people to decide what NOT to do.

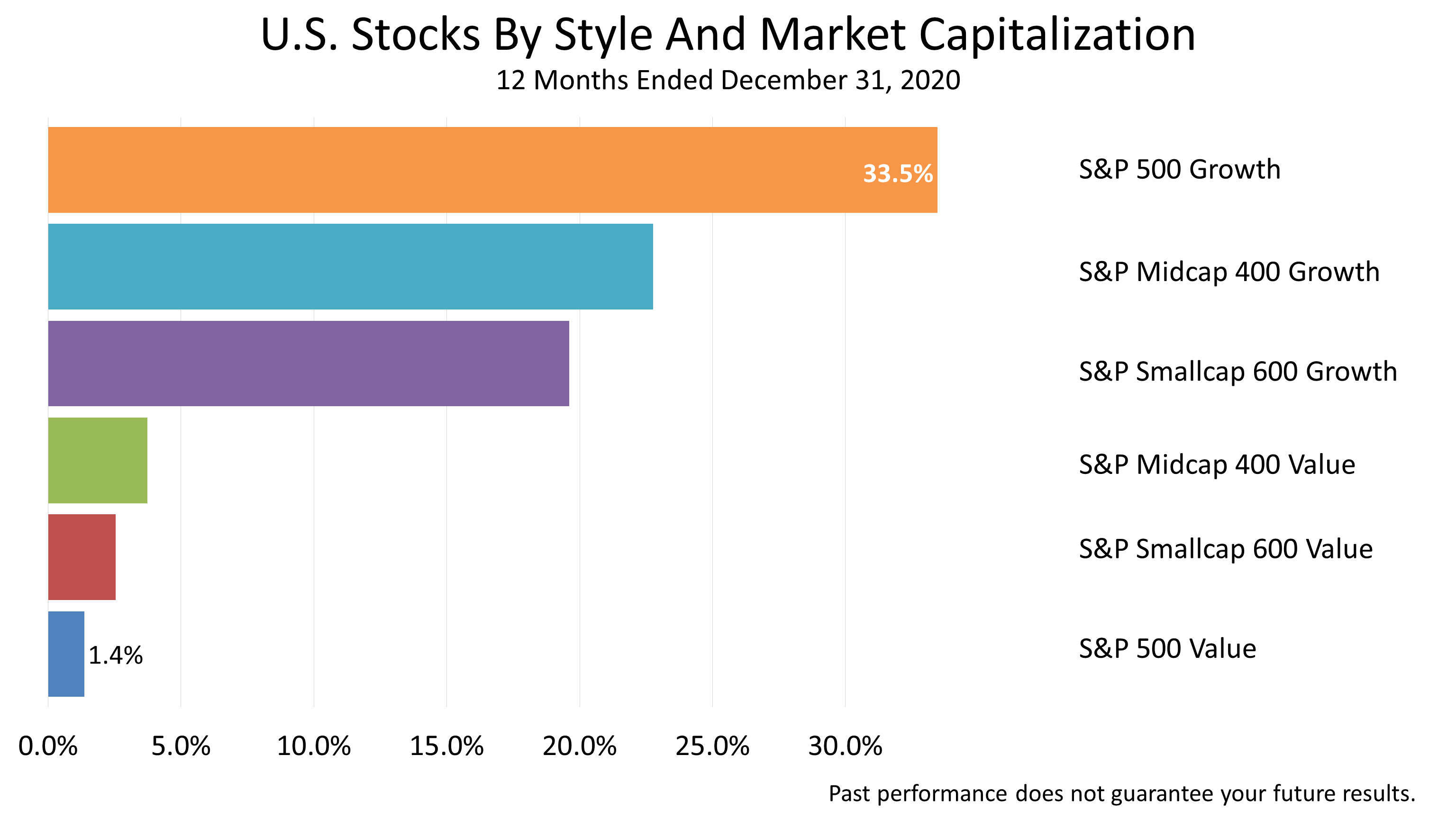

Click image to enlarge

You can see the huge difference in performance between growth and value style stocks, where the large growth stocks literally returned more than 20 times the +1.4% on large-cap value stocks.

These changes in market leadership—and in laggards—are not predictable.

Pinpointing exactly when they will happen cannot be done reliably.

This is a rare case when, as a professional, you learn enough to know you do not know enough to predict markets accurately.

The smart way to deal with this as an advisor is to stick with the basics, like modern portfolio theory (MPT).

Click image to enlarge

Modern portfolio theory is a large body of financial knowledge based on academic research done over the last 70 years.

This approach does not guarantee success—nothing can. It’s called a theory because your investment results can’t be guaranteed.

However, it is assuring to know that this framework for investing is now taught in the world’s best business schools and embraced by institutional investors.

Click image to enlarge

Modern portfolio theory (MPT) is a framework for managing investment risk based on financial, economic, and statistical facts.

Classifying investments based on distinct statistical characteristics imposes a quantitative discipline for managing assets based on history and fundamental facts about the economy.

Click image to enlarge

While MPT is a good quantitative basis for evaluating investment risk, the world is too dynamic and not enough statistical history exists to make predictions with any certainty about which investments will outperform in the months ahead.

Human judgment and an understanding of historical performance is critical in applying modern portfolio theory.

Applying modern portfolio theory also requires periodically lightening up proportionately on the most-appreciated types of assets and buying more of the types of assets that lagged. The exact amount of each asset is set based on personal preferences, age, and specific circumstances.

Click image to enlarge

The Chinese stock market led major world stock market indexes in the 12 months ended December 31, 2020.

But comparing the Chinese stock market to U.S., European, and Asian Pacific equities markets is kind of an apples and oranges comparison.

The U.S. and other free-market economies in Japan and Europe are not government manipulated.

The Chinese stock market is a fraction of the size and offers a fraction of the liquidity of the U.S. equities markets.

China's public companies do not have the institutional strength and history of public accounting in the United States.

The risk of Chinese stocks was recently highlighted by the case of Chinese billionaire Jack Ma, who reportedly was once the richest man in the country.

He is the cofounder and former executive chairman of Alibaba Group, a multinational technology conglomerate.

Ma is also a strong proponent of an open and market-driven economy.

He resurfaced in January after a three-month vanishing act, which just happened to follow a speech critical of Chinese regulation of business.

It’s kind of like what would happen if Jeff Bezos were mysteriously to disappear for three months after publicly criticizing the President.

Point is, the Chinese economy and market are very different from the U.S., and that needs to be the lens you use to filter the Chinese stock market index data shown here.

Click image to enlarge

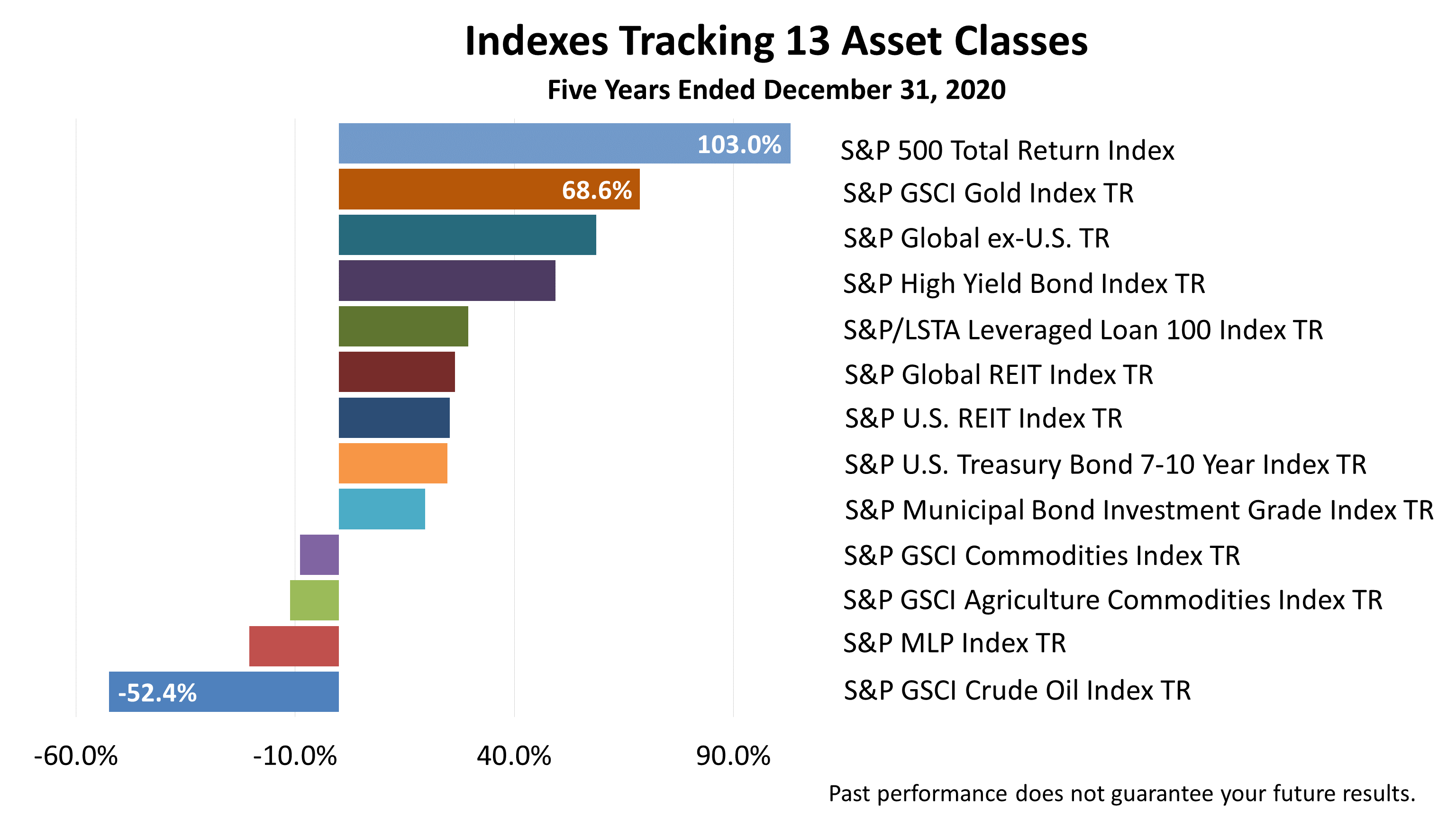

Comparing the performance of 13 asset classes, a wide array of different investments for the past year, can you spot any unusual trends?

What stands out is gold.

Gold has been a terrible investment for years and years.

It is a hedge against inflation, but there is no evidence of inflation on the horizon.

It is also a hedge against currency risk and financial crisis.

There is a limited supply of gold.

Gold plays a role in a diversified portfolio, but it is a bit role. It’s not a leading player.

Click image to enlarge

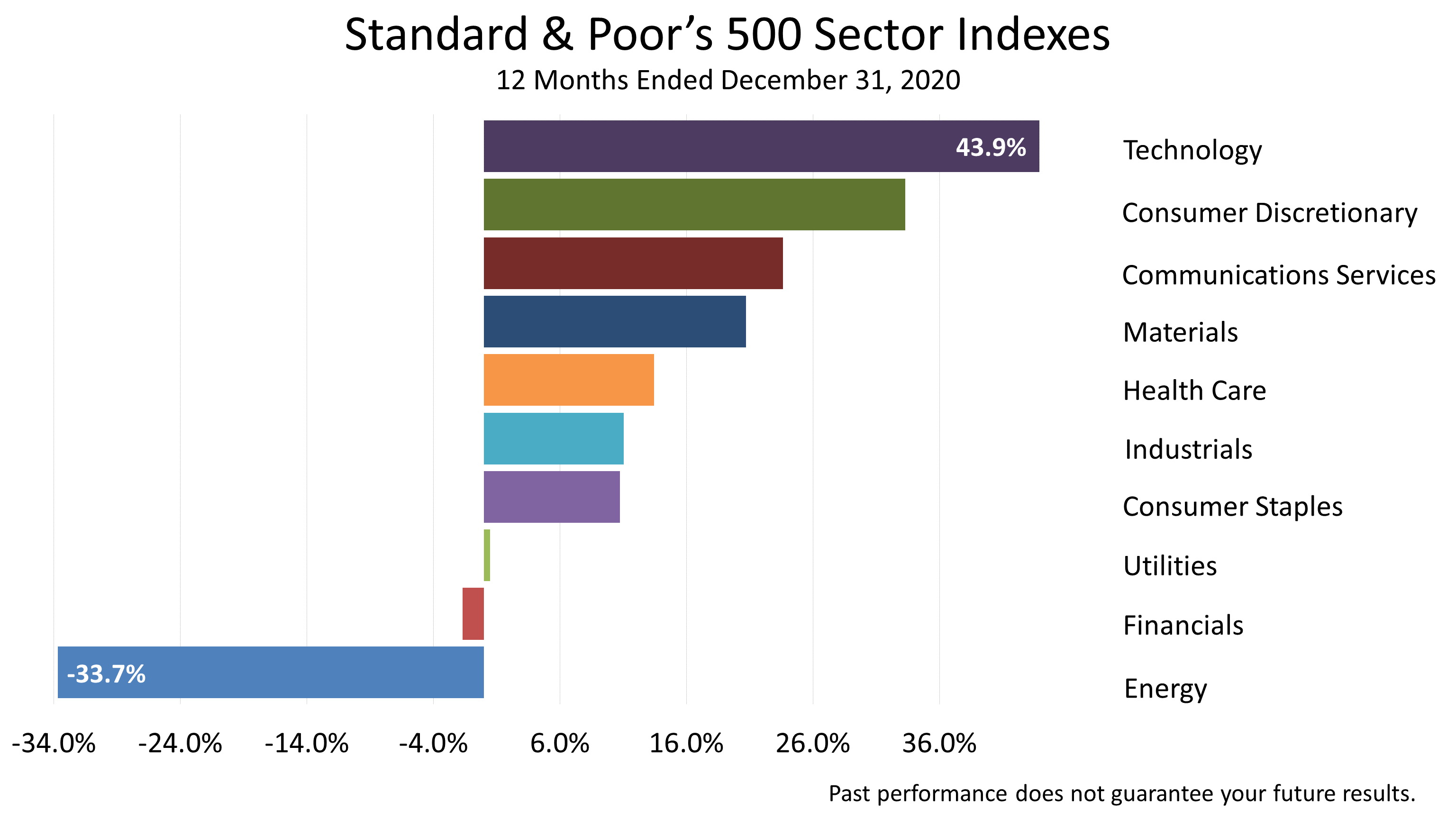

Looking at stock investments by industry over the 12 months ended December 31st, 2020, tech stocks were the winners. Again.

Propelled by the FAANG stocks—Facebook, Amazon, Apple, Netflix, Google—U.S. equities, when examined though a lens filtered by industry sectors, outperformed all other industry sectors.

The pandemic drove profit growth for the FAANG stocks.

While smaller companies—private, local, independently owned businesses with a few employees, along with small-cap public companies—trailed the FAANG-driven technology industry sector of the S&P 500, the last quarter did hold some promise for broadening of the economic expansion.

Click image to enlarge

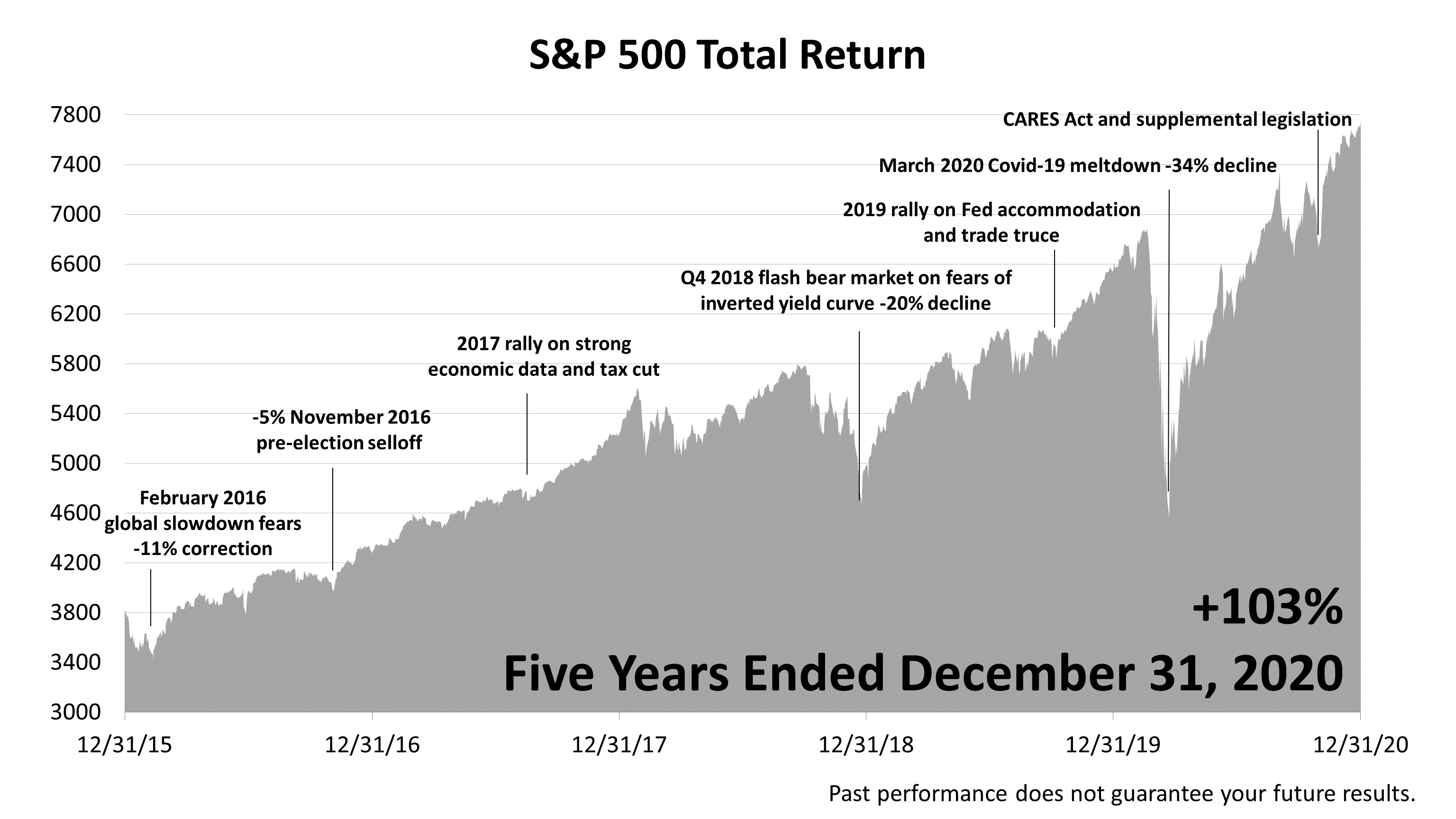

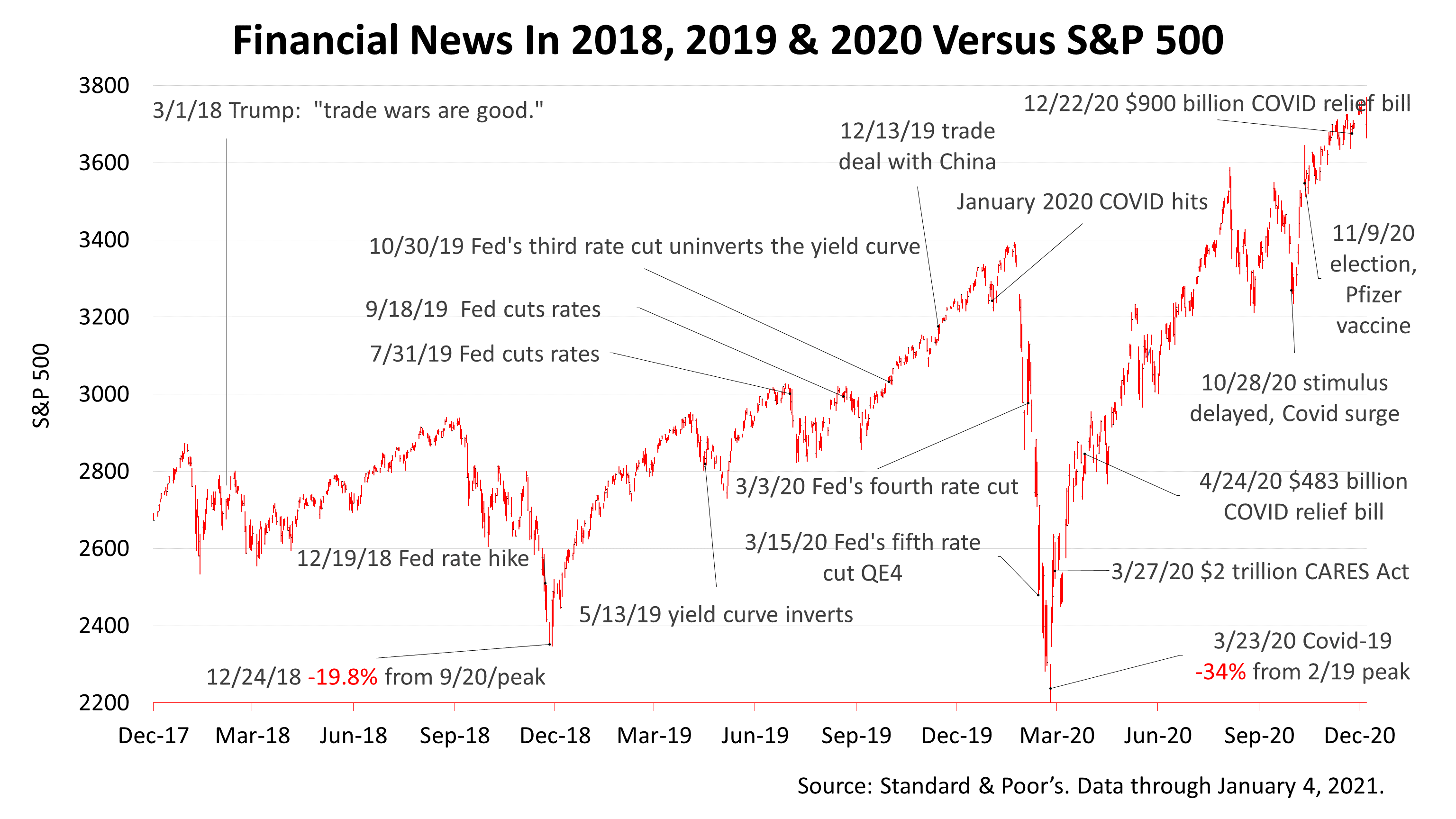

Do you feel like the last five years have gone by fast?

Let’s review.

After trading sideways for approximately two years in 2015 and most of 2016—hitting two air pockets along the way—the stock market broke out after the November 2016 election.

Stocks—a key growth component in a diversified portfolio—rose steadily to an all-time peak on September 20, 2018.

Then it dove by -20% on fears that an inverted yield curve was imminent.

On January 4, 2019, the Fed signaled rates were on hold, whereupon stocks rallied for most of the remainder of 2019.

In February of 2020, stocks hit a new all-time peak; then Covid-19 put the economy into a recession and stock prices dropped a jaw-dropping -33.9%!

As violent as was the plunge, so too was the economic and stock price recovery.

By early September of 2020, stocks hit a record all-time high following the enactment of CARES and related legislation.

After a pause, stocks rallied steadily from the November 2020 election through year-end.

This was a very busy five years.

Over the last five years, including dividends, the S&P 500 total return index has gained +103%.

Click image to enlarge

Click image to enlarge

Click image to enlarge

Click image to enlarge

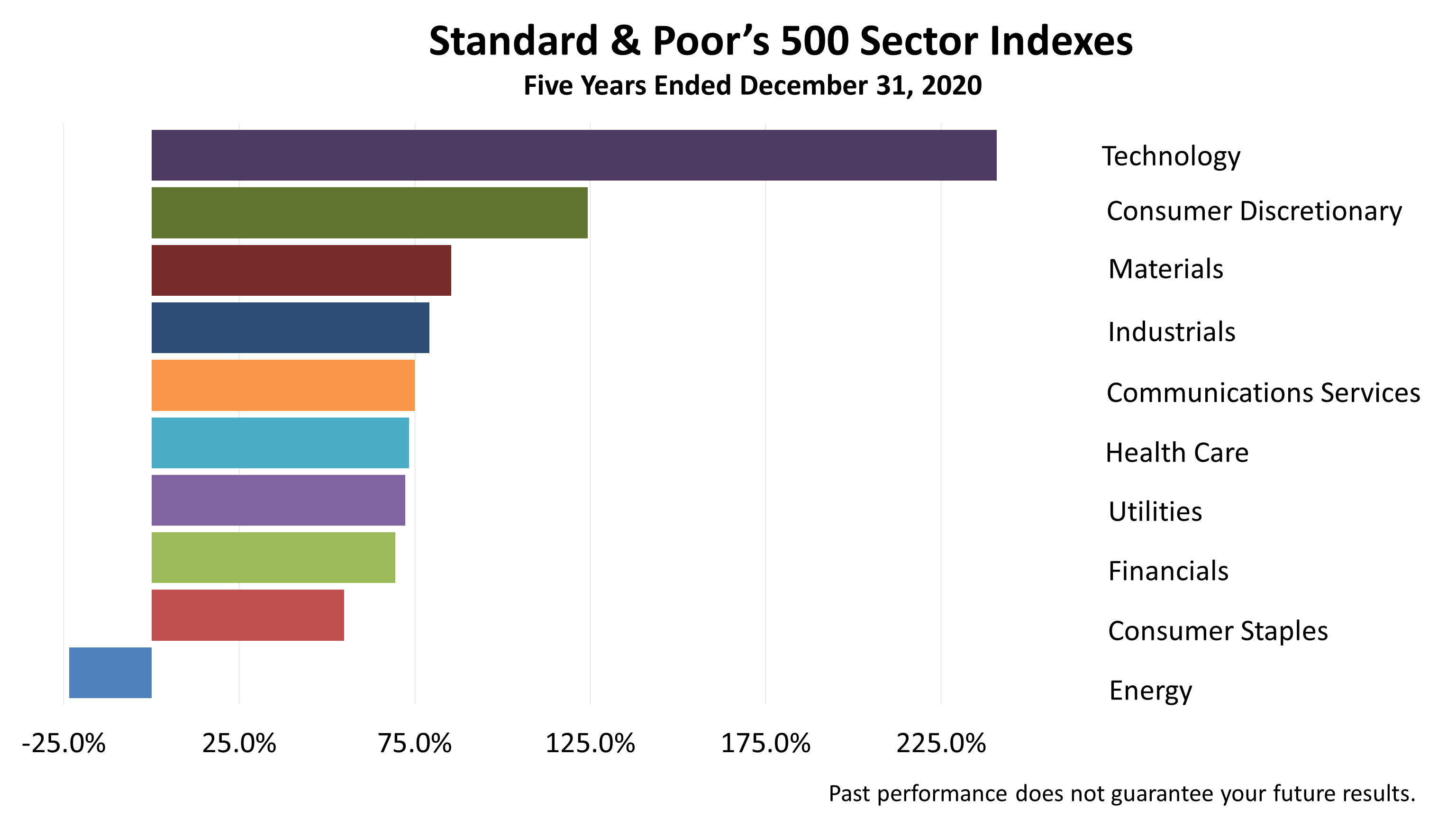

Across a diverse group of 13 asset classes, what stands out is the five-year doubling in value of the S&P 500.

Stocks normally average a +10% return annually.

Doubling that annually for the past five years is amazing, especially when you consider the events of the past five years.

Click image to enlarge

Look at the major financial news in just the last three years that ended on December 31, 2020.

A trade war with China in March 2018, the -20% quick bear market at the end of 2018, a yield curve inversion at the end of 2019, a string of five rate cuts, a pandemic -34% bear market, and about six trillion dollars of government relief and more on the way—all of which adds to the debt to be paid by the next generation.

It’s a lot.

And now stocks are hitting new highs because investors are anticipating a lot of fiscal stimulus.

Not only the $900 billion in additional Covid relief, but lots more to come, very likely, with the new administration.

Notwithstanding the events of January 6th, the market just keeps marching higher on the theory that we're going to see one heck of an economic recovery once most of us get vaccinated.

So, I guess, in a nutshell, that's what I think the market has been doing.

Click image to enlarge

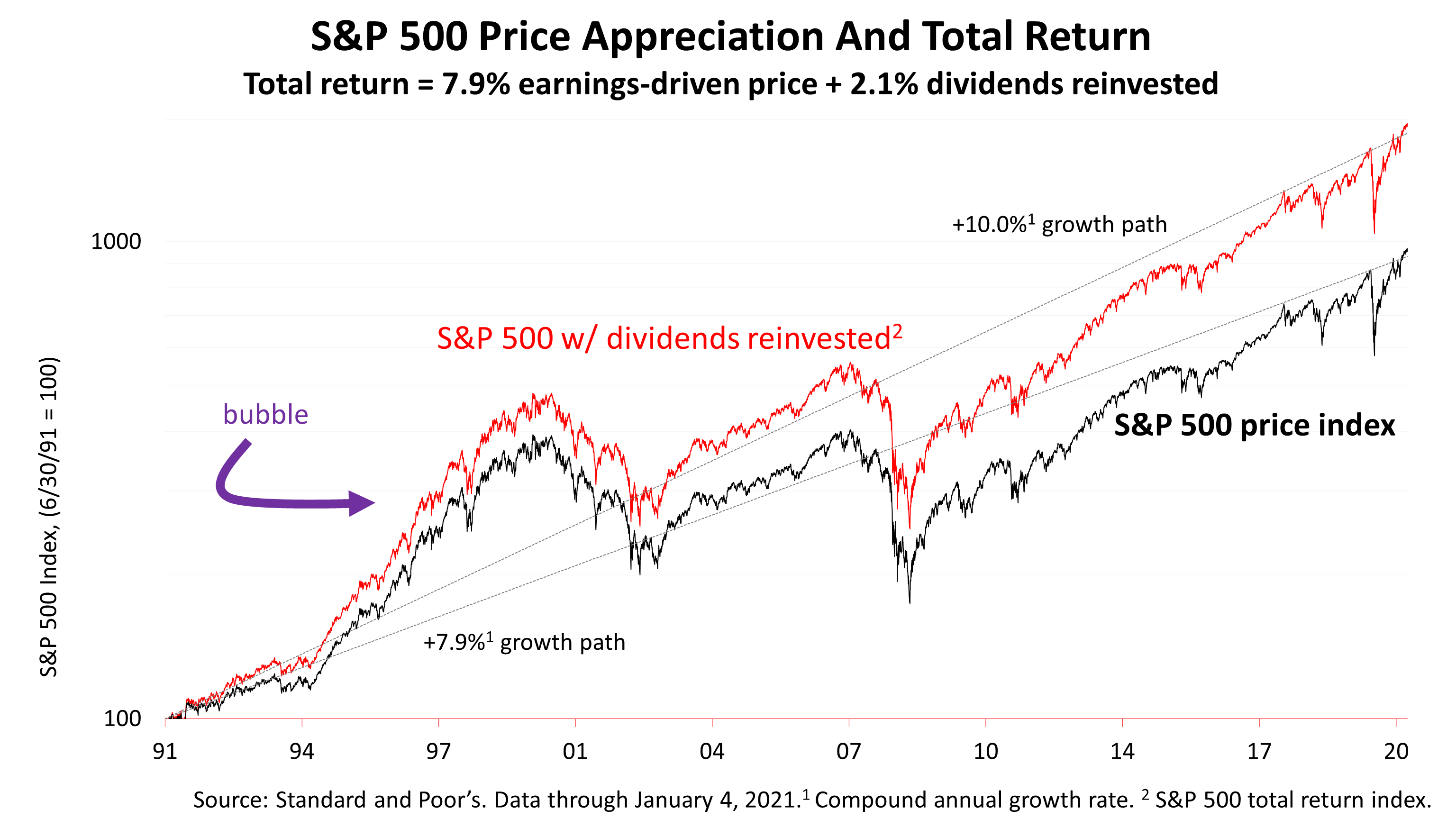

Is the stock market overvalued?

The stock market, ever since March of ’09, has been converging with the long-term +10% rate of appreciation.

And +10% is actually the total return going back as much as 200 years of U.S. financial history.

You can see what a real bubble looked like when things really got out of whack, truly got out of whack.

You can see how high above this long-term trend rate of appreciation the stock market had become, whereas today you don't see anything like that.

I just find this chart so useful in the current context, when people are talking “bubble” and “overvaluation.”

Now, you could quibble and say, “Well, yeah, but we are ahead of the long-term trend.”

I wouldn’t argue with that; there is room for the stock market to trade off.

But I’m just saying, in round numbers, stocks are pretty much where one would expect them to be, given 200 years of U.S. financial history during which stocks have returned about +10% compounded annually.

Click image to enlarge

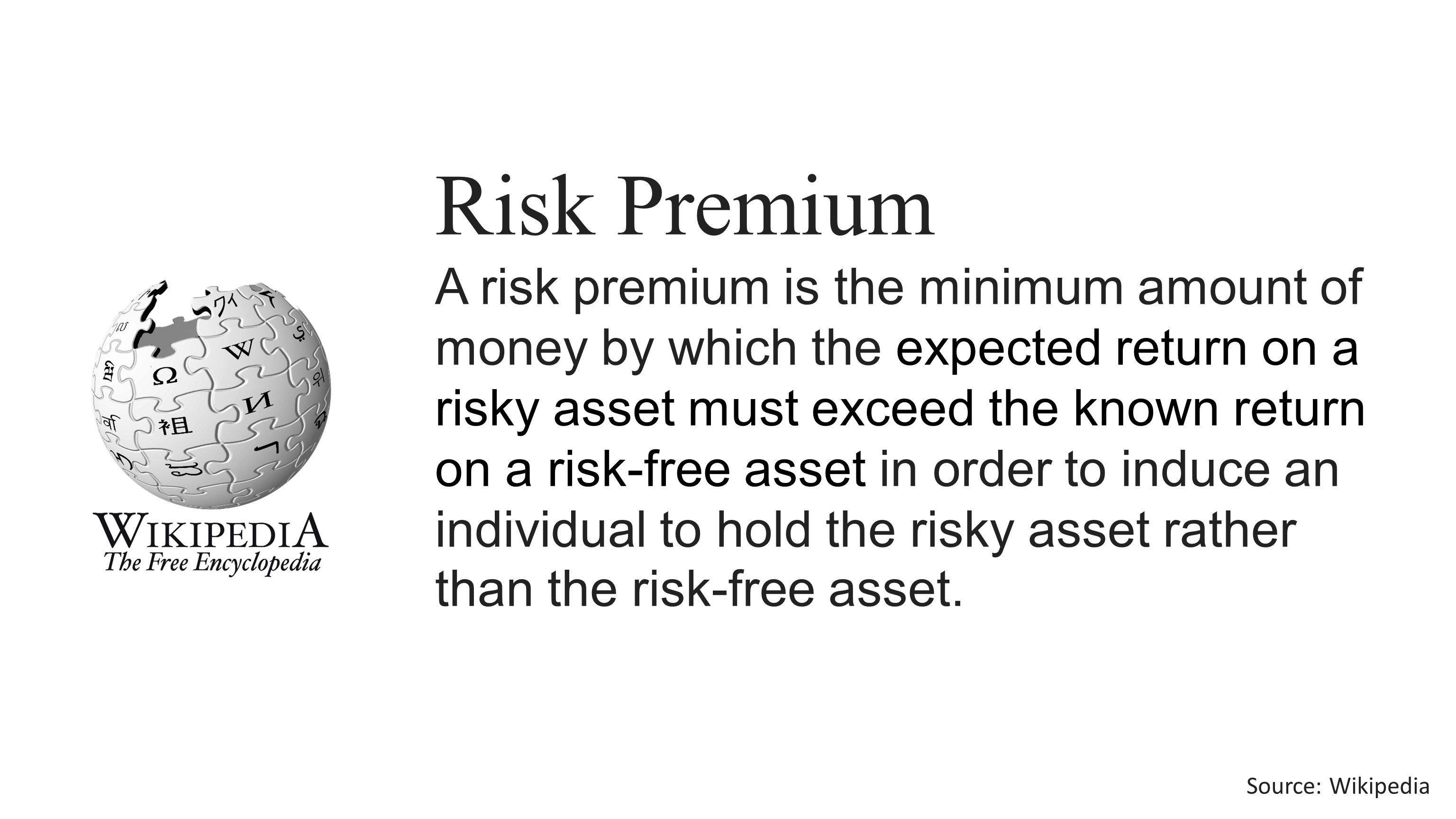

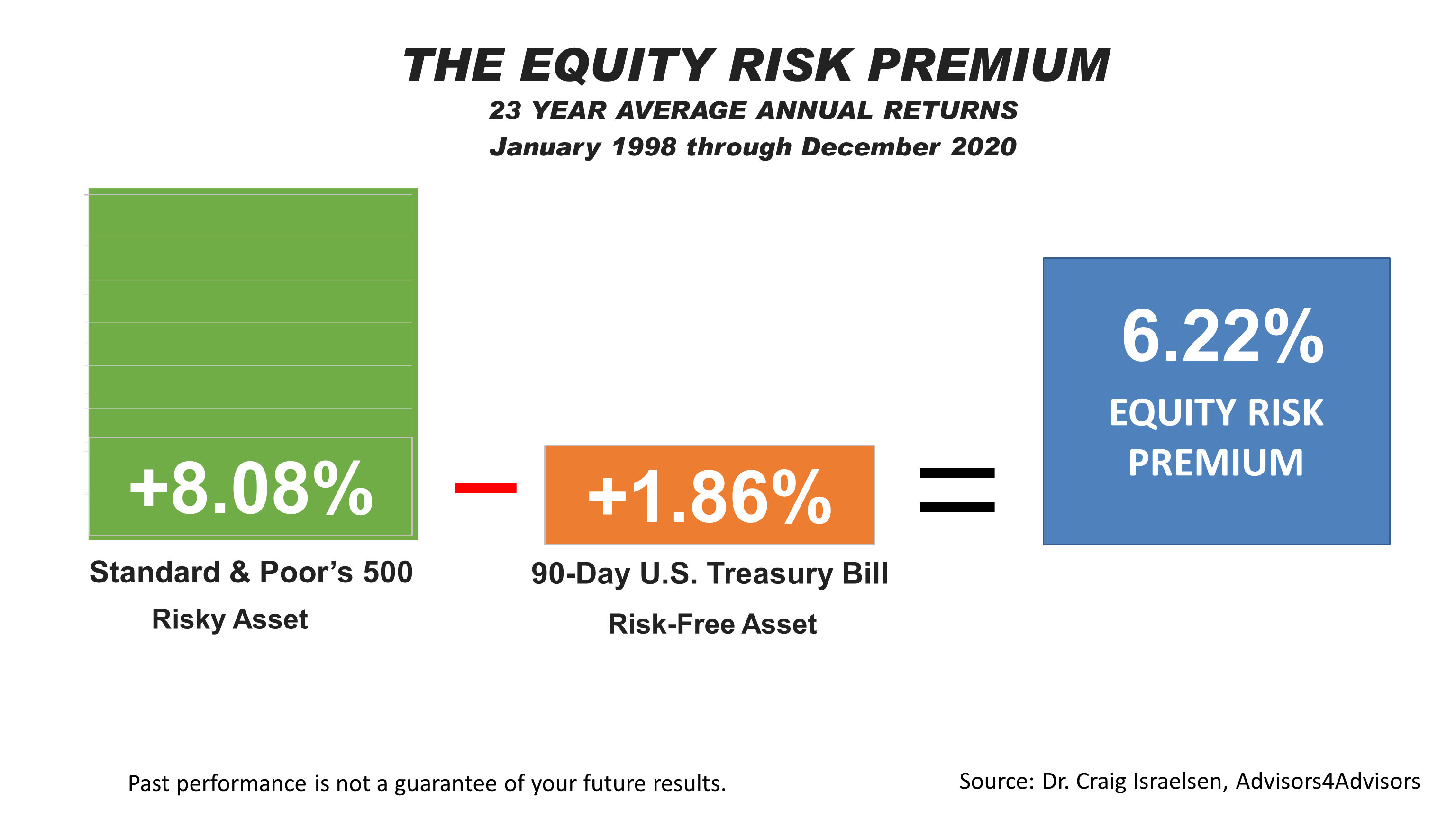

A rubric of modern portfolio theory holds that investors get paid extra return for taking risk.

The risk premium is the amount you get paid for owning a risky asset.

Click image to enlarge

To quantify the equity risk premium, here are the numbers: Over the 23 years ended on December 31, 2020, the risk-free 90-day U.S. Treasury bill averaged an annual return of +1.86%, compared to a +8.08% annualized return on the S&P 500 stock index.

By subtracting the 1.86% from the 8.08%, we quantify the premium stock investors have been paid as +6.22% annually over the boom and bust cycles since 1998.

Owning stocks through the tech bubble in 2000, financial crisis in 2008 and 2009, and the COVID bear market rewarded investors with a premium of 622 basis points over what they would have earned by investing in risk-free 90-day Treasury

The equity risk premium fattened considerably in the last quarter, moving from +5.75% to +6.22% as the return on stocks improved while the 90-day Treasury bill remained incredibly low.

Low Treasury bill rates and the stimulus have created a mountain of cash.

Click image to enlarge

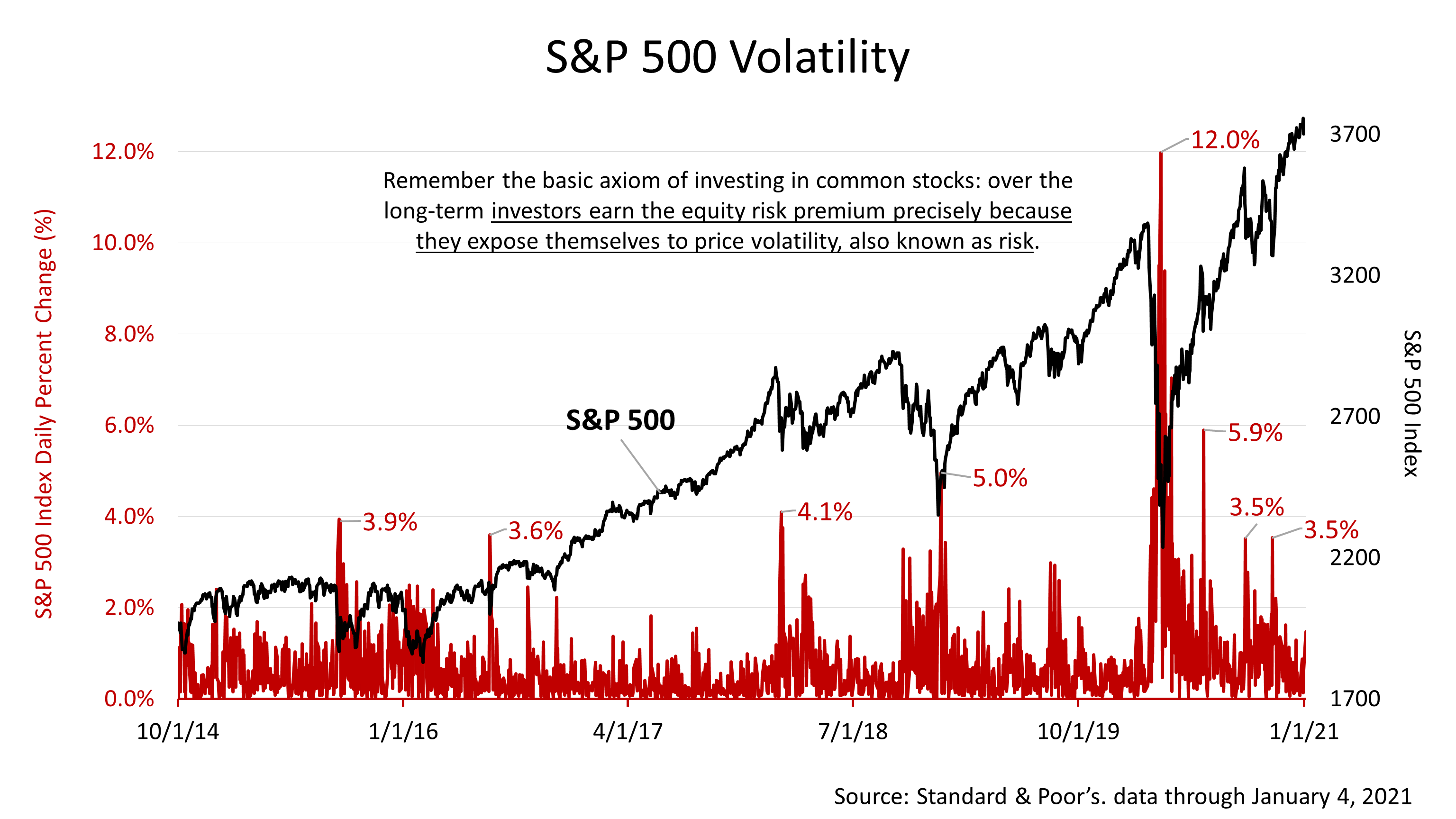

This chart does a better job of illustrating the scary part of the equity risk premium.

The red data series shows the daily changes in the stock market, as represented by the S&P 500.

Big one-day drops of between -3% and -5% are not uncommon, and earlier this year we had a single-day plunge of -12%!

So, indeed, earning the equity risk premium is hard and scary at times.

But again, if we're just armed with these kinds of statistics, which show that big daily down days do come frequently and almost like clockwork, it is easier to withstand the uncertain times.

With the COVID outbreak continuing and the worsening hospitalization rate across many states, the risk of a stock market plunge should be expected, but retirement investors – permanent investors who plan to own stocks for the rest of their lives – would be wise to view volatility as a friend.

That's a different way of looking at the world, but it absolutely is valid.

Choosing to expose a portion of your portfolio to price volatility, also known as risk, enables you to earn a better return over the long run.

You wouldn't earn the 6-percentage-point equity risk premium in stocks if you weren't exposed to lots of volatility.

It just goes with the territory. It’s part of owning a risk asset.

Click image to enlarge

Times of painful stock market losses are when investors actually earn the equity risk premium, and that’s an important financial fundamental to remember in times like these.

Click image to enlarge

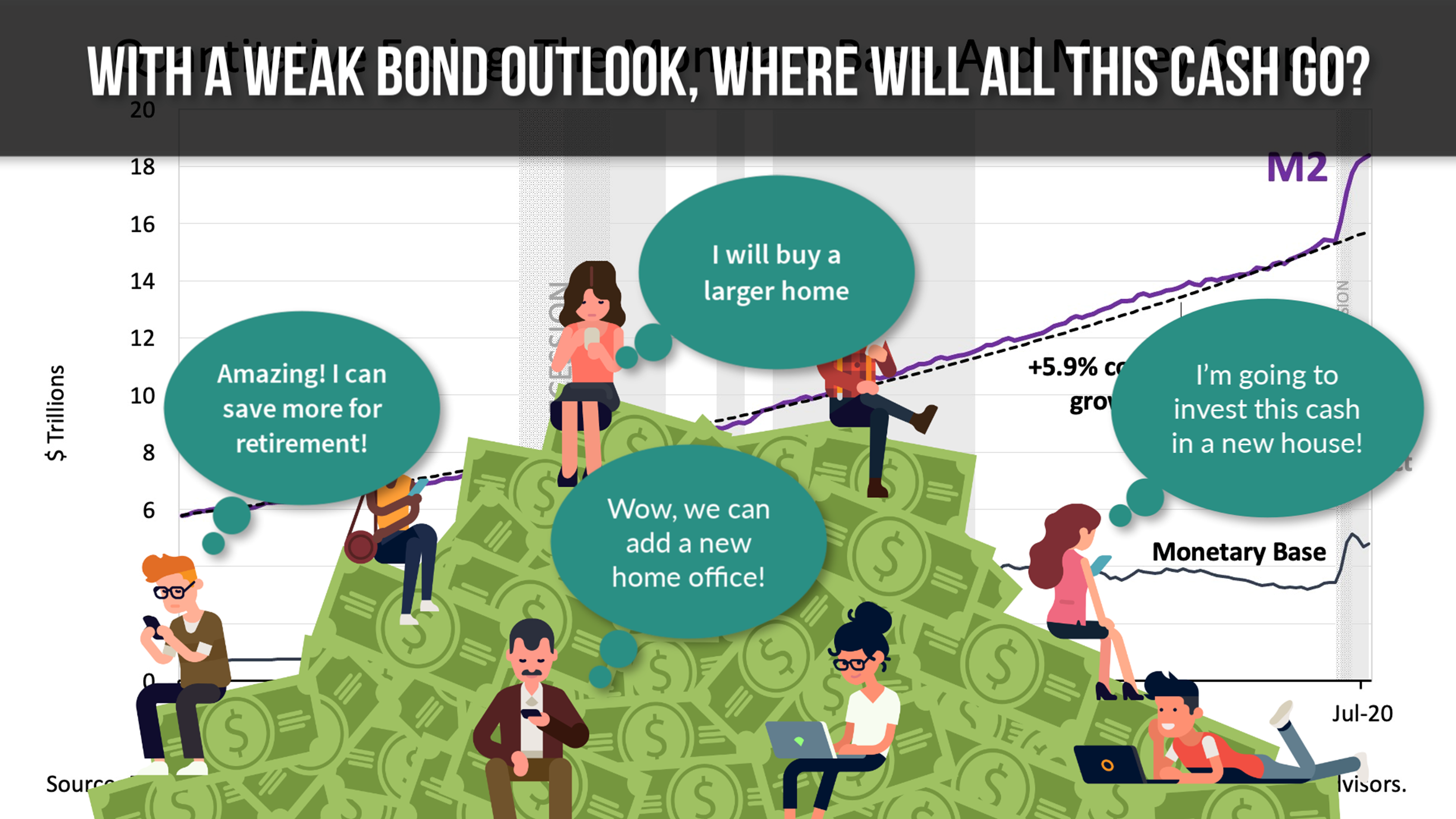

With the cloud of Covid hanging heavy across the nation, Americans are sitting on an unprecedented mountain of cash.

M2, the money supply, a statistic no one has cared about since Paul Volcker ran the Federal Reserve in the late 1970s, has exploded!

If ever there were a silver lining, it’s that staying at home has enabled Americans to amass a cash reserve as never before.

It’s confounding! In 2020, the nation endured perhaps the worst trauma and drama of the post-War era. Deaths from Covid are breaking tragic records not expected to peak after Christmas, a political schism amid an information revolution is tearing apart the political fabric of the nation, but stock prices have repeatedly broken new, all-time-record highs!

What is going on?!

Click image to enlarge

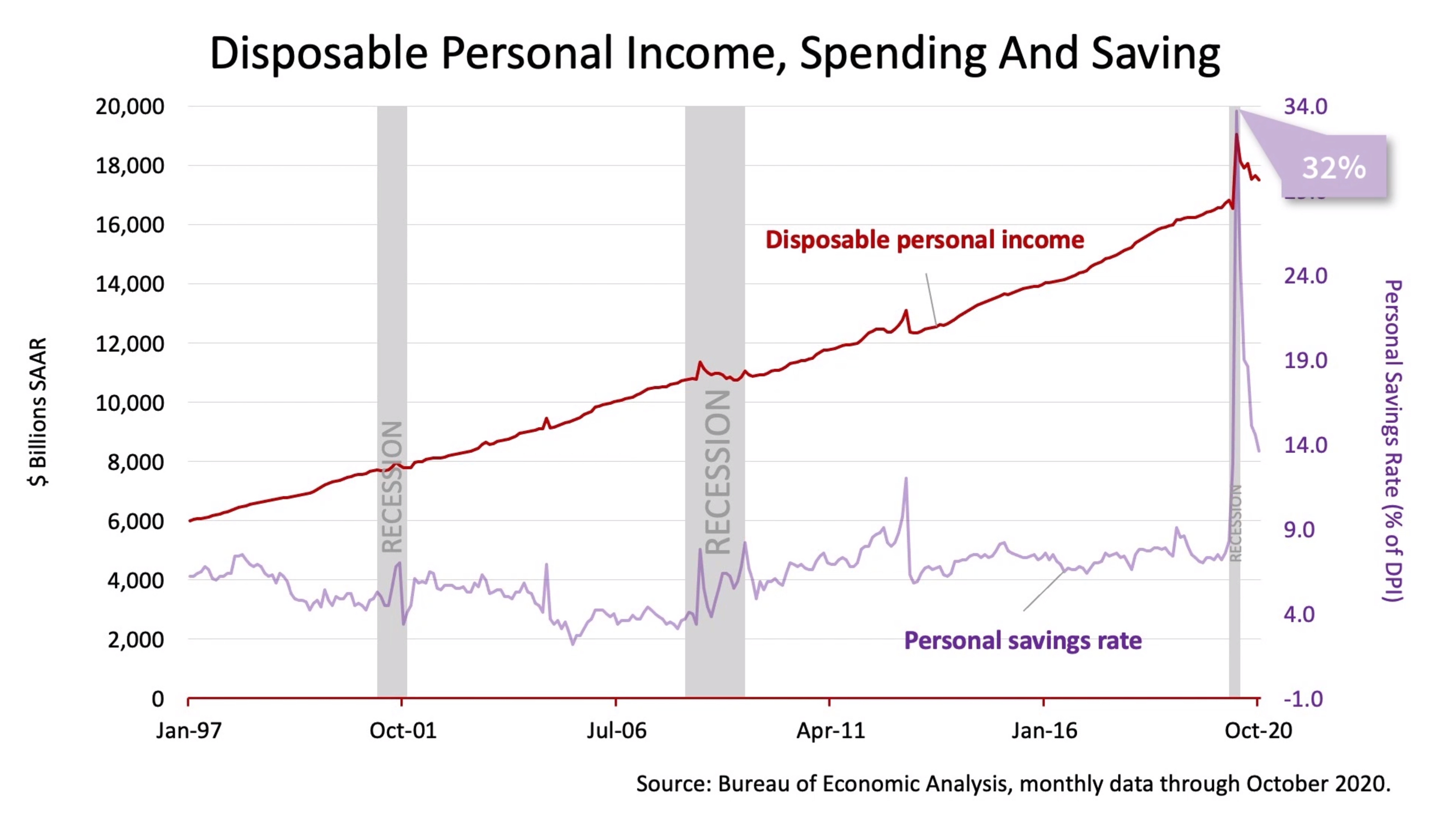

Back in April, disposable personal income was sent skyrocketing by emergency Covid aid in the CARES Act.

That also sent personal savings surging to a once-unfathomable rate of +32%!

The savings rate has been coming back toward normal since April, but very slowly, and THAT’S created this huge cash hoard.

Turns out, instead of spending all that cash on restaurants, vacations, and entertainment, consumers have been banking it, leaving the savings rate much higher than normal since April.

Keep in mind, the higher-than-normal savings rate has been going on, month after month, since April, and the effect is cumulative: The pile of cash being saved keeps growing month after month!

What’s that mean?

Click image to enlarge

Money supply, also known as M2, which consists of currency held by the public plus checking, savings, and money market accounts, has skyrocketed like never before in modern times!

With interest rates low and the Fed saying it is not planning to raise rates for the foreseeable future, bonds are not an attractive investment.

So, consumers sitting on this mountain of cash that has been mounting for months now may see no better place to put the savings glut than into stocks and housing.

Central bankers and economists will be debating the long-term effects of the growing influence of government in the U.S. economy and the risk it poses, but the financial outlook for now is unexpectedly bright, even as the dark cloud of the pandemic casts a long shadow over the nation.

Click image to enlarge